Last reviewed: July 2026

Most investing advice is about what to do. Almost none of it is about when. And timing — not in the market-timing sense, but in the sense of sequencing financial decisions correctly relative to your life stage — is where a significant amount of value gets lost or created.

The most consistent timing mistake Jeff sees: people applying accumulation strategies during the preservation phase, and preservation strategies during the accumulation phase. The strategies aren’t wrong in the abstract. The timing is wrong.

Key Takeaways

- Applying the right strategy in the wrong life stage costs more than picking the wrong strategy.

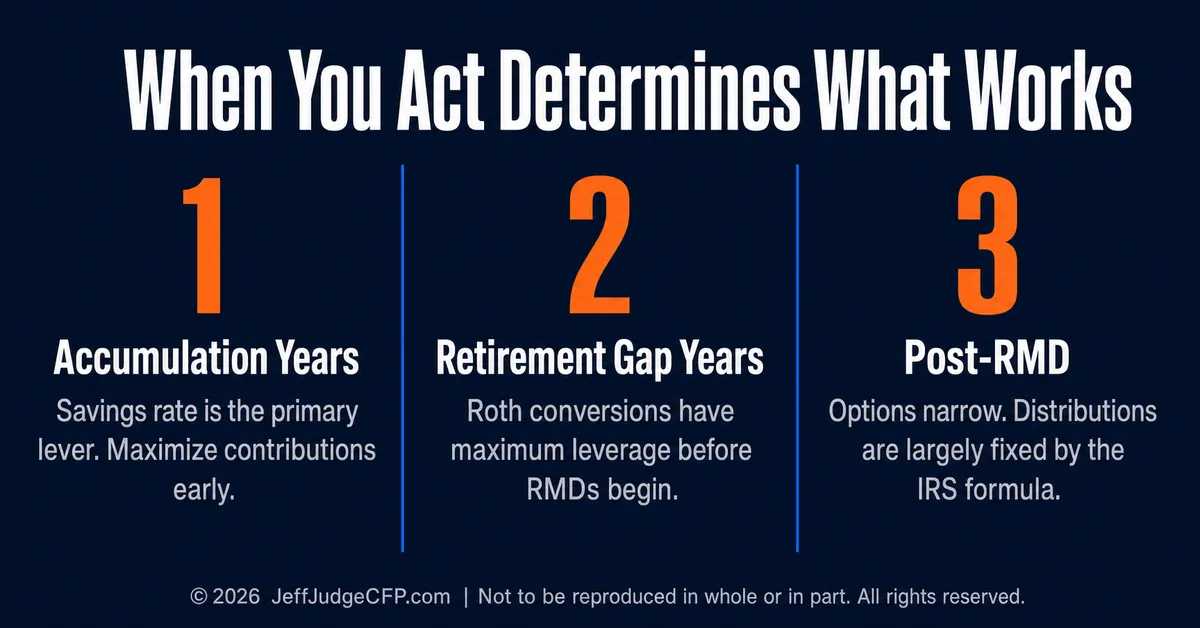

- Three windows have different levers: accumulation (savings rate), the gap years (Roth conversions), and post-RMD (limited).

- Per the IRS, RMDs begin at age 73; the gap before then is the most leveraged window for conversions.

- Per the SSA, delaying Social Security from 62 to 70 raises the monthly benefit by roughly 77% for those born after 1960.

- Per the IRS, 2026 brackets run 10% to 37%, so the Roth-versus-traditional choice is mostly about timing your rate.

About the Author

About the Author: Jeff Judge, CFP®, AEP®, ChFC®, CLU® is a financial planner who writes Viewpoints for JeffJudgeCFP.com. He helps families and business owners match each move to the right window in the accumulation-to-distribution cycle, using the R.U.D.D.E.R. Method™, the financial planning process Jeff developed. “The most common mistake I see isn’t a wrong strategy. It’s the right strategy applied in the wrong window, like preserving capital that still has 15 years to grow.”

When Does Timing Matter More Than Strategy?

Several of the most consequential financial decisions aren’t really decisions about strategy at all. They’re decisions about timing. Getting the sequence right is what creates the value.

| Decision | Why Timing Determines the Outcome | When It Has Maximum Leverage |

|---|---|---|

| Roth vs. traditional contributions | Lower bracket now = Roth wins; higher bracket now = traditional wins | During lower-income years relative to projected retirement rate |

| Roth conversions | Each converted dollar is taxed at today’s rate, not retirement’s | Early retirement gap before RMDs begin at 73 |

| Tax-loss harvesting | Losses offset gains; more valuable in high-gain years | Years with concentrated position sales or major capital events |

| Social Security claiming | Permanent decision affecting 20-30 years of income | Requires modeling 3-5 years before retirement, not day-of |

| Conservative allocation shift | Sequence-of-returns risk applies to early withdrawal years, not accumulation years | The first 5-7 years of retirement, not the decade before |

The Roth vs. traditional decision is primarily a timing decision. Per the IRS, the 2026 marginal tax brackets run from 10% to 37%. If you’re currently in the 22% bracket and expect to be in the 32% bracket in retirement, the Roth wins. If you expect the reverse, the traditional account wins. The strategy is identical. The timing determines the outcome.

Equity compensation timing often matters more than portfolio allocation. For people with significant unvested RSUs or stock options, the decision of when to exercise, which grants to prioritize, and how to handle the tax event from vesting often has more financial impact in a given year than the portfolio allocation below it.

Is choosing Roth or traditional really a timing decision?

Largely, yes. Per the IRS, 2026 brackets run from 10% to 37%. If your rate today is lower than the rate you expect in retirement, Roth wins; if it is higher, traditional wins. The contribution type is the same; the timing of when you pay the tax decides the outcome.

What is the early retirement timing window most people ignore?

The three planning windows in most people’s financial lives have different primary levers. Understanding which window you’re in determines which moves have maximum impact.

| Window | Approximate Age Range | Primary Lever | Why It’s the Right Move Here |

|---|---|---|---|

| Accumulation phase | 30s to late 50s | Savings rate, tax-advantaged contributions, equity growth | Compounding has maximum runway; volatility has time to recover |

| Retirement gap | Early retirement to age 73 | Roth conversions, Social Security claiming, withdrawal sequencing | Income is controllable before RMDs force a fixed distribution schedule |

| Post-RMD phase | 73+ | Qualified charitable distributions, asset location | Options narrow; IRS formula largely sets the distribution schedule |

The gap between early retirement and age 73, when required minimum distributions begin per the IRS, is one of the most financially leveraged windows in most people’s financial lives. Income in this period can often be managed more intentionally than at any other time.

Roth conversions in this window take advantage of lower income in early retirement to prepay tax at a lower rate before forced distributions begin. A person who retires at 62 has 11 years to execute conversions before the RMD schedule takes over and income becomes less manageable.

Social Security claiming timing permanently affects every year of retirement income. Per the Social Security Administration, delaying from age 62 to 70 increases the monthly benefit by roughly 77% for someone born after 1960. That’s a permanent difference that interacts with Roth conversion timing, Medicare IRMAA thresholds, and withdrawal sequencing in ways that require planning before retirement, not after.

Why are the years between retirement and 73 so valuable?

Because income is most controllable then. Before Social Security, pensions, and RMDs stack up, you can convert to Roth and sequence withdrawals at lower rates. Someone who retires at 62 has about 11 years to act before the RMD schedule, per the IRS, fixes much of the income.

Frequently Asked Questions

Does timing matter more than strategy in financial planning?

Often, yes. The same strategy can help or hurt depending on when you use it. Applying accumulation moves in the preservation phase, or preservation moves while still accumulating, is a more common and costly error than choosing a flawed strategy in the first place.

What are the three financial planning windows?

Accumulation, roughly your 30s to late 50s, where savings rate and growth lead; the retirement gap, from retiring to age 73, where Roth conversions and Social Security timing have the most leverage; and the post-RMD phase, 73 and up, where the IRS formula narrows your options.

When should you shift to a conservative allocation?

Generally around the first five to seven years of withdrawals, when sequence-of-returns risk peaks, not a decade before. A 48-year-old planning to retire at 63 still has about 15 years of compounding ahead, so a heavy bond shift then can be 10 to 15 years premature.

How much does delaying Social Security increase the benefit?

Per the Social Security Administration, delaying from age 62 to 70 raises the monthly benefit by roughly 77% for someone born after 1960. Because it is permanent and interacts with conversions and IRMAA, the claiming decision should be modeled three to five years before retirement, not on the day.

What is the timing mistake Jeff sees most often?

People in their peak earning years — their 40s and early 50s — who are prioritizing conservative investment strategies because retirement “feels close.” The logic feels sound: preserve what you’ve built. The practical consequence is that they’re applying a preservation mindset to capital that still has 15 to 25 years of compounding ahead of it.

A 48-year-old who shifts to a 40% equity allocation because retirement feels imminent may be making that shift 10 to 15 years early. The sequence-of-returns risk that justifies a more conservative allocation applies to the early years of withdrawal — not to the years of accumulation 15 years before the first withdrawal.

Per Bureau of Labor Statistics data, the median retirement age in the U.S. sits around 62 to 65 for most workers. A 48-year-old planning to retire at 63 still has 15 years of compounding ahead. The capital in their portfolio today needs to work hard for another decade and a half before preservation logic applies to most of it.

The strategy isn’t wrong. It’s being applied in the wrong window.

Schedule a no-obligation call with Jeff to review whether your current strategy is timed correctly for where you actually are in the accumulation-to-distribution cycle.

The information provided is for educational purposes only and should not be construed as investment advice. Investment strategies should be tailored to individual circumstances, risk tolerance, and goals. Past performance doesn’t guarantee future results. Consult with qualified financial professionals regarding your specific situation. Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through Great Valley Advisor Group, a registered investment advisor and separate entity from LPL Financial. © 2026 JeffJudgeCFP.com | Not to be reproduced in whole or in part. All rights reserved.