Last reviewed: July 2026

The age-based asset allocation formula has been embedded in retirement planning advice for decades. 100 minus your age in stocks. Or 110 minus your age. Or 120 minus your age, as the formula has evolved with longer life expectancies. The premise is that your risk exposure should automatically decline as you age, producing a progressively more conservative portfolio as retirement approaches.

This is a rule of thumb masquerading as a financial plan. And for many high earners with substantial assets and long time horizons, it’s pointing in the wrong direction.

Key Takeaways

- Age-based formulas like 100 minus your age in stocks are rules of thumb, not financial plans.

- Two people the same age can need very different allocations; one may warrant 60-75% equity, another 35-50%.

- Per the SSA, a 65-year-old today has roughly a one-in-three chance of reaching 90, demanding more growth, not less.

- A high earner retiring at 58 who follows 100-minus-age holds about 42% equity, dangerously low for a 35-year horizon.

- Allocation should follow portfolio income reliance, time to first withdrawal, real risk tolerance, and purpose, not age.

About the Author

About the Author: Jeff Judge, CFP®, AEP®, ChFC®, CLU® is a financial planner who writes Viewpoints for JeffJudgeCFP.com. He helps families and business owners set allocation from income needs, time horizon, and purpose rather than a birthday, using the R.U.D.D.E.R. Method™, the financial planning process Jeff developed. “Age is a convenient proxy because it’s one number you can look up. It’s a poor one because it ignores everything that actually drives how your portfolio should behave.”

Why doesn’t age-based asset allocation work as a rule?

What it gets right: The general direction. As you approach the period when you need to draw on your portfolio, having less of it in volatile assets reduces sequence-of-returns risk. That part is sound logic.

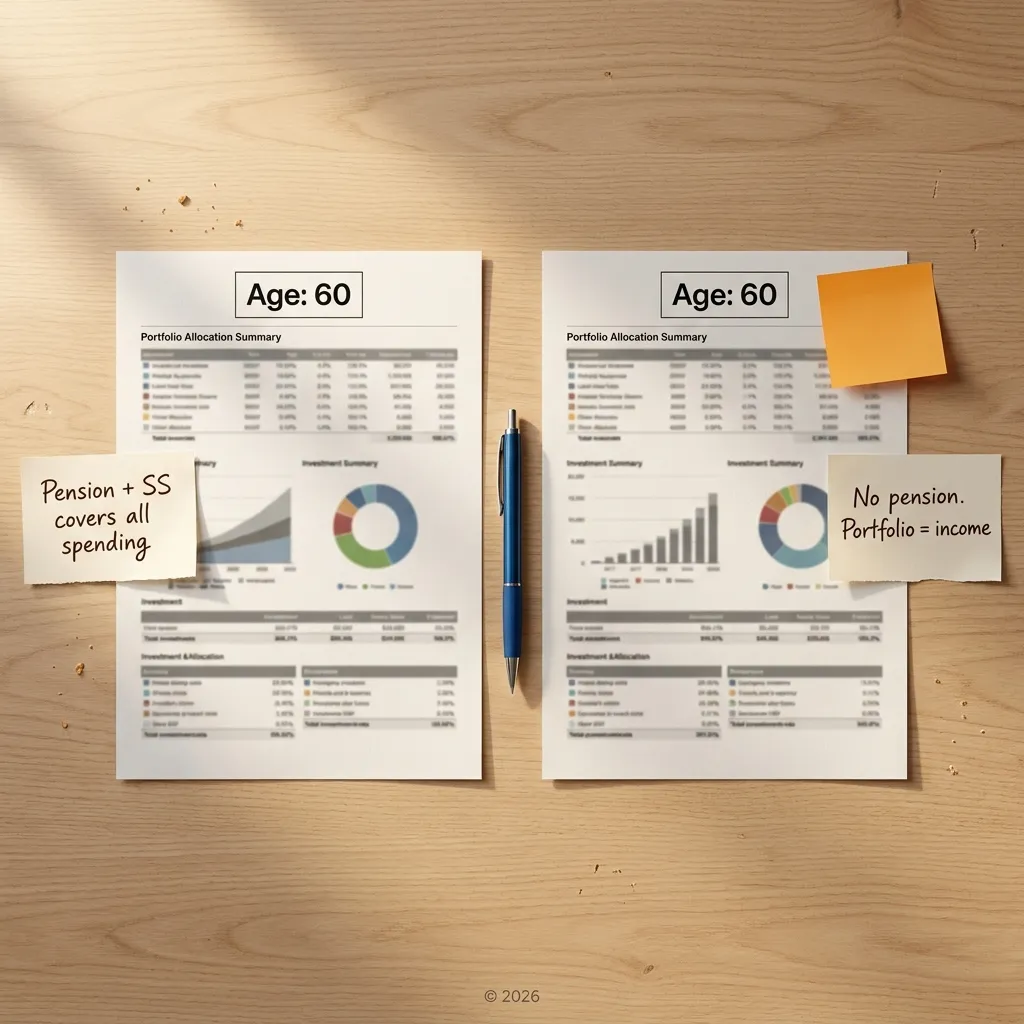

What it gets wrong: The assumption that age determines risk tolerance and allocation need. Two people at age 60 with identical ages have wildly different financial situations.

| Factor | Retiree A, Age 60 | Retiree B, Age 60 |

|---|---|---|

| Formula equity allocation (100 minus age) | 40% | 40% |

| Pension income | Yes, covers 85% of expenses | None |

| Portfolio income reliance | Low; portfolio is supplemental | High; primary income source |

| Time to first major draw | 10+ years | 3 years |

| Portfolio’s primary purpose | Growth and legacy | Income starting at 63 |

| Appropriate equity range | 60-75% | 35-50% |

The formula says they should have identical allocations. They shouldn’t. One has a pension as a buffer; the other is the pension.

Does your age actually determine the right stock allocation?

Not on its own. Age is a convenient single number, but two 60-year-olds can have opposite needs. One with a pension covering most spending can hold more equity; one whose portfolio is the income source needs a larger bond buffer. What the money has to do matters far more than how old you are.

The longevity problem: The Social Security Administration reports a 65-year-old today has approximately a one-in-three chance of living to age 90. A couple where both are 65 has better than a 50% chance that at least one reaches 90. Per the formula, a 65-year-old in 1950, with an average life expectancy of about 78, might have reasonably held 35% in equities. A 65-year-old today planning for a 30-year retirement may need substantially more equity exposure to avoid running out of money.

How does the formula specifically fail high earners?

High earners who retire early are the clearest case. Someone who retires at 58 and follows the 100-minus-age formula holds 42% equities. But they have a 30 to 35 year time horizon and no pension. They need growth. A 42% equity allocation in year one of a 35-year retirement is dangerously conservative for this profile.

High earners with significant other income sources represent the opposite problem. A 68-year-old with pension income, Social Security, and rental income that covers all spending has zero forced reliance on the investment portfolio for near-term income. The formula says 32% equities. But this person’s portfolio doesn’t need to provide income — it needs to preserve and grow wealth for heirs or late-stage care. An equity allocation considerably higher than 32% may be appropriate.

Investment accounts held for estate planning purposes should not be allocated based on the owner’s age. If the portfolio is intended to pass to the next generation, the relevant time horizon is the heir’s, not the owner’s remaining life expectancy.

Should estate-bound money be invested for your age or your heirs’?

For your heirs. Money you intend to leave behind carries the beneficiary’s time horizon, which may be decades longer than your own. Allocating it conservatively based on your age can needlessly cap growth on assets that will not be spent in your lifetime.

Frequently Asked Questions

Is the 100-minus-your-age rule good advice?

It captures one true idea, that risk should ease as you near drawing on the portfolio, but it fails as a plan. The rule assumes age alone sets your needs. Two people the same age, one with a pension and one without, should hold very different allocations.

Why is age-based allocation often wrong for high earners?

Because their situations diverge from the average. A high earner retiring at 58 who follows 100-minus-age holds about 42% equity for a 35-year horizon, too conservative. Another with a pension covering all spending could hold far more equity than the formula’s 32%, since the portfolio is for growth and legacy.

How does longevity change the right allocation?

Longer lives need more growth. Per the Social Security Administration, a 65-year-old today has roughly a one-in-three chance of reaching 90, and for a couple the odds at least one does exceed 50%. Planning a 30-year retirement on a mid-century equity level risks running short.

What should set your asset allocation instead of age?

Four inputs replace age: how much of your spending the portfolio must fund, how long until major withdrawals begin, how you would truly behave in a 30% decline, and whether the money is for income, legacy, or both. Together they describe what your portfolio actually needs to do.

What should determine your allocation instead?

Four factors replace age as the meaningful inputs:

| Factor | What to Measure | What the Answer Tells You |

|---|---|---|

| Portfolio income reliance | What percentage of spending must the portfolio fund? | Higher reliance = more conservative buffer warranted in early withdrawal years |

| Time to first major withdrawal | When does significant drawing begin? | Longer runway = more time for volatility to recover |

| Real risk tolerance | How would you act in a genuine 30% decline? | Determines whether higher equity exposure is actually sustainable |

| Portfolio’s ultimate purpose | Income, legacy, or both? | Legacy-focused portfolios often support longer effective time horizons |

A person with pension and Social Security covering 100% of their income need can hold a high equity allocation throughout retirement. A person whose portfolio is the primary income source needs more bond exposure to buffer against sequence-of-returns risk in the early withdrawal years. Neither answer has anything to do with age.

Age is a convenient proxy for these inputs because it’s a single number that’s easy to look up. It’s a poor proxy because it ignores everything that actually determines how your portfolio should behave.

Schedule a no-obligation call with Jeff to build an allocation based on your actual situation rather than a formula that doesn’t know anything about you.

The information provided is for educational purposes only and should not be construed as investment advice. Investment strategies should be tailored to individual circumstances, risk tolerance, and goals. Past performance doesn’t guarantee future results. Consult with qualified financial professionals regarding your specific situation. Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through Great Valley Advisor Group, a registered investment advisor and separate entity from LPL Financial. © 2026 JeffJudgeCFP.com | Not to be reproduced in whole or in part. All rights reserved.