One of the stranger conversations Jeff Judge has with clients involves people who have, by any reasonable measure, already won.

They have more than enough. Retirement is funded. Kids are through college. House is paid off. And they’re still anxious. Still checking the portfolio twice a day. Still feeling vaguely unsatisfied when the market goes sideways. Still measuring themselves against a number that keeps moving.

That’s the scoreboard problem. The number on the screen stopped being a goal and became a scoreboard, and the scoreboard is always playing another game.

Why the Scoreboard Problem Happens

Investment accounts are designed to feel like scoreboards. The balance changes daily. Percentage gains and losses are displayed prominently. Benchmarks sit in the background. The whole interface is built for engagement, which means it’s built to make you feel like something is always at stake.

That’s appropriate when you’re building toward a goal. It’s actively unhelpful when you’ve reached one.

The scoreboard becomes a habit. People who spent thirty years watching the number go up find it genuinely difficult to stop watching, even when the number no longer needs to go anywhere in particular. The anxiety about the score remains long after the game is over.

There’s also a social dimension Jeff sees often in his practice. Clients compare themselves to peers, to headlines, to whatever the market returned last quarter. The scoreboard attaches to relative performance, not personal sufficiency. Your portfolio can be doing exactly what it needs to do for your life while “losing” by the scoreboard’s measure. That’s not a financial problem. It’s a framing problem.

How to Know If You Have the Scoreboard Problem

Here’s the diagnostic question Jeff runs with clients who show signs of scoreboard thinking: “If your portfolio dropped 20% tomorrow, what would actually change in your life?”

For most people with the scoreboard problem, the honest answer is: nothing immediate. They wouldn’t need to delay retirement. They wouldn’t have to change their spending. The number would be lower, and that would feel terrible, but it wouldn’t change anything real.

The feeling of threat, in those cases, is the scoreboard talking. Not the actual plan.

A few clear signals that the scoreboard has taken over:

- You check the portfolio more than once a day, outside of scheduled review periods

- A good market day improves your mood; a bad one ruins it, regardless of your actual financial position

- You feel behind, even though you have no specific target you’re behind on

- You adjust your allocation based on recent returns rather than your plan

Any one of these is worth paying attention to. All four together is the scoreboard problem running at full speed.

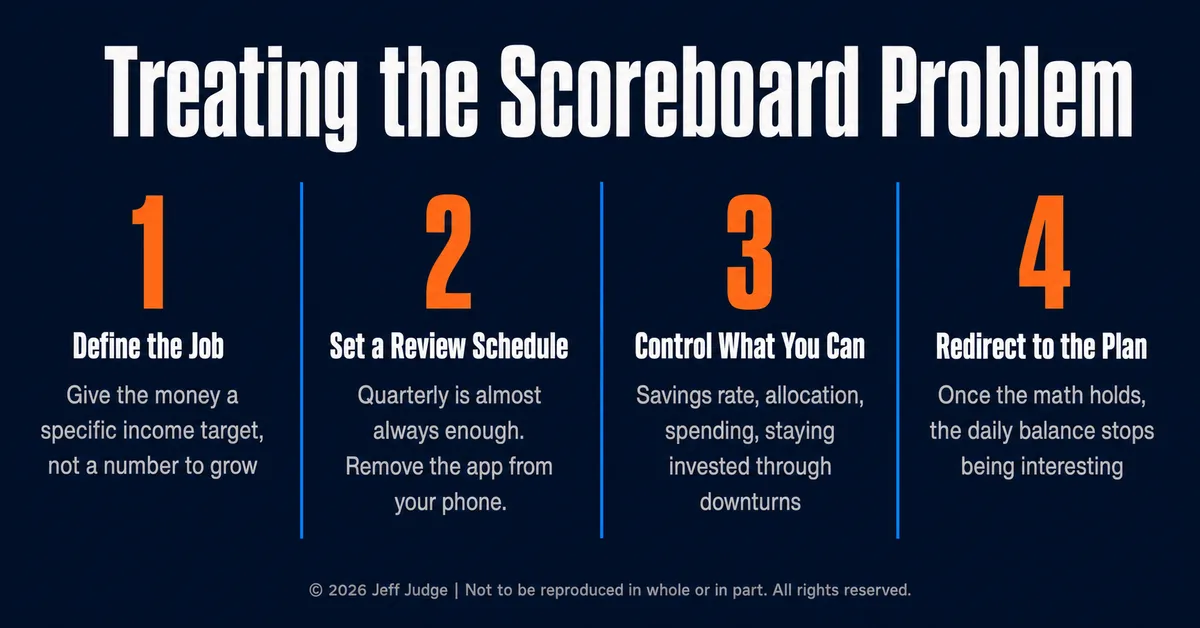

How to Treat the Scoreboard Problem: A Four-Step Process

Step 1: Define what the money actually needs to do

Give the portfolio a specific job. Not “grow as much as possible.” Something concrete: “Fund $7,500 a month in retirement spending, starting at age 64, for 30 years.” A specific job description makes the daily score irrelevant to most decisions.

According to the Social Security Administration, the average monthly Social Security benefit for a retired worker at age 62 in 2026 is $2,969. Most people need their portfolio to supplement that figure, not replace it entirely. Knowing the exact gap between your Social Security income and your actual spending target is the first step in turning a scoreboard into a plan.

Step 2: Set a review schedule and stick to it

Quarterly reviews are almost always sufficient for long-term investors. Monthly reviews are reasonable for people early in retirement. Daily reviews serve almost no useful purpose and cause considerable psychological harm. Remove the app from your home screen if you need to.

Step 3: Separate what you can control from what you can’t

You can control your savings rate, your allocation, your spending, and whether you stay invested during downturns. You can’t control daily market returns, inflation, or what your neighbor’s portfolio did. Scoreboard thinking conflates these categories. A sound plan puts your attention on the controllable variables and stops there.

Step 4: Redirect attention from the balance to the plan

What does the balance need to do? What’s the actual spending rate? What’s the actual risk you can’t afford to take? Once those questions have concrete answers, the daily balance becomes much less interesting. Which is exactly where you want it.

What the Goal of Financial Planning Actually Is

The goal isn’t a large number. It’s a plan that works under realistic conditions, that you understand well enough to stick with, and that gives you the specific confidence of knowing the math holds.

Jeff has watched this play out with clients across multiple market cycles. The people who sleep well aren’t the ones with the most money. They’re the ones who stopped watching the scoreboard because they know their plan doesn’t depend on today’s score.

That’s a meaningful distinction, and it doesn’t happen by accident.

If you can describe, in plain English, what your portfolio needs to produce and when, and you know the math holds even in a rough market, the daily balance stops being interesting. That’s the treatment.

Schedule a no-obligation call with Jeff to build the plan that makes the scoreboard irrelevant.

,-

The information provided is for educational purposes only and should not be construed as investment advice. Investment strategies should be tailored to individual circumstances, risk tolerance, and goals. Past performance doesn’t guarantee future results. Consult with qualified financial professionals regarding your specific situation.

Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through Great Valley Advisor Group, a registered investment advisor and separate entity from LPL Financial.

Chesapeake Financial Planners | © 2026 JeffJudgeCFP.com | Not to be reproduced in whole or in part. All rights reserved. | (410) 652-7868 | www.chesapeakefp.com

§