A high income is not a financial plan. It’s a larger margin for error. And for a surprising number of high earners, that margin gets used up on lifestyle rather than wealth. The result: six-figure income, thin net worth, and a retirement that requires either a dramatic lifestyle cut or a very late exit from work.

The income trap: why high earners underperform on wealth

The conventional wisdom is that wealth follows income. Work hard, earn more, and financial security follows naturally. This is one of the most expensive assumptions in personal finance.

The Bureau of Labor Statistics Consumer Expenditure Survey shows that household spending tracks income closely at every level. People who earn more spend more, and they spend more across virtually every category. That’s not surprising. What is surprising is how little of the income difference compounds into net worth.

The mechanism is lifestyle creep. Every raise, promotion, or income increase comes with a corresponding spending adjustment that feels proportional and justified in the moment. The bigger house that fits the neighborhood. The schools. The cars that reflect where you are professionally. None of it is irrational on its own terms. Collectively, it consumes the income that was supposed to become wealth.

5 traps that keep high earners from building real wealth

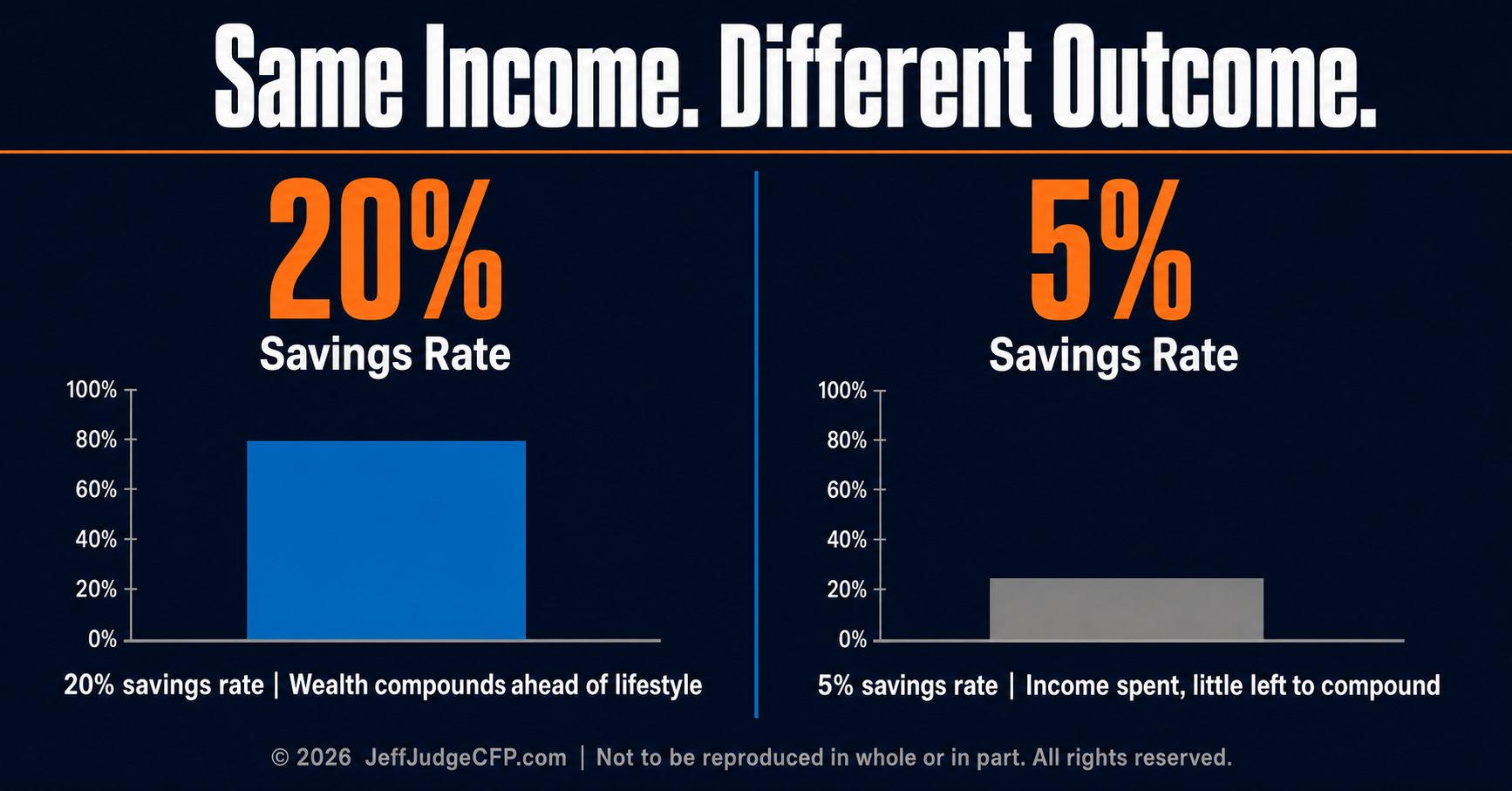

1. Optimizing income at the expense of savings rate. The highest earners spend enormous energy on career optimization, negotiation, and income growth while giving almost no attention to their savings rate. A person earning $300,000 with a 5% savings rate is building wealth more slowly than a person earning $120,000 with a 20% savings rate. Income is the input. Savings rate is the lever.

2. Delaying investment until “things calm down.” High earners often have complex financial situations: equity compensation, deferred income, variable bonuses, business interests. The complexity becomes a reason to delay systematic investing. A year of delay in a tax-advantaged account costs the compounding on every year that follows.

3. Using future income to justify current spending. The expectation of continued high income is treated as a current asset. The mortgage that requires two strong incomes to service. The lifestyle built on a bonus that hasn’t arrived yet. This works right up until it doesn’t.

4. Ignoring tax drag on wealth accumulation. Per the IRS, the top marginal federal income tax rate in 2026 is 37%, kicking in at $626,350 for single filers and $751,600 for married filing jointly. At those income levels, every dollar of avoidable tax is a dollar that isn’t compounding. High earners who don’t run a coordinated tax strategy are routinely giving back $40,000 to $80,000 or more per year in taxes that competent planning could have avoided or deferred.

5. Confusing high income with financial sophistication. High earners often assume their professional success translates to financial acumen. It doesn’t. These are different skills. The confidence gap between how financially sophisticated high earners think they are and how financially sophisticated they actually are is one of the most consistent patterns in financial planning practice.

https://res.cloudinary.com/dmfujved8/image/upload/v1778795922/uc_alsznh.png

{kind=link}

What the net worth number actually tells you

Net worth is the honest measure. Income is what you make. Net worth is what you kept, grew, and didn’t spend.

A household earning $250,000 at age 50 with a net worth of $400,000 has a problem. Not a cash flow problem. A wealth problem. That $400,000 cannot sustain the lifestyle that $250,000 in income has been funding. The gap between the lifestyle they’ve built and the portfolio that needs to fund it in retirement is the actual risk.

The people who catch this early enough to fix it usually do so because someone made them calculate it, not in the abstract, but with actual numbers attached to their actual spending and their actual retirement date.

Jeff has had this conversation enough times to recognize the look that happens when someone runs the numbers for the first time and realizes the income they were so focused on optimizing was running about 20 years behind the wealth they were supposed to be building.

The fix isn’t income. It’s the math you haven’t run yet.

The path forward for high earners isn’t complicated. It’s uncomfortable. It requires treating the savings rate with the same intentionality as the income, running an actual retirement income projection against actual spending, and building a tax strategy that recovers some of what’s been given back unnecessarily.

None of that requires a lifestyle cut in the near term. It requires a decision that the current income is building something, not just funding something.

What percentage of your gross income went to savings and investment last year? If you don’t know that number, that’s the gap.

Schedule a no-obligation call with Jeff to run the actual numbers on your income-to-wealth trajectory.

,-

The information provided is for educational purposes only and should not be construed as investment advice. Investment strategies should be tailored to individual circumstances, risk tolerance, and goals. Past performance doesn’t guarantee future results. Consult with qualified financial professionals regarding your specific situation.

Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through Great Valley Advisor Group, a registered investment advisor and separate entity from LPL Financial.

© 2026 JeffJudgeCFP.com | Not to be reproduced in whole or in part. All rights reserved.

§