Net worth is the number most high earners track as a proxy for financial progress. Hitting $1 million, then $2 million, then some imagined finish line feels like the right metric. It isn’t. Net worth is an asset minus liability snapshot. It doesn’t tell you whether you can retire, when, or what that retirement actually looks like. There’s a different number that does, and most people have never calculated it.

That number is your financial independence ratio: the percentage of your annual spending that your portfolio can permanently replace without depleting the principal.

What is the financial independence ratio?

The calculation: Take your current invested assets (not including primary home equity, which produces no income). Multiply by your sustainable withdrawal rate, a conservative estimate is 3.5 to 4%, depending on your timeline. Compare that annual income figure to your actual annual spending. The ratio of portfolio-generated income to spending tells you where you are on the path to financial independence.

Why it’s more useful than net worth: A person with $2 million in invested assets and $200,000 in annual spending has a 3.5% withdrawal generating $70,000, covering 35% of their spending. They’re 35% of the way to financial independence. A person with $1.2 million in invested assets and $60,000 in annual spending generates $42,000, covering 70% of their spending. Despite lower net worth, they’re nearly twice as far along the path.

The Social Security modifier: Per the Social Security Administration, the average monthly benefit for a retired worker in 2026 is $2,071. For a married couple where both spouses receive benefits, the average household Social Security income approaches $4,000 to $5,000 per month. That guaranteed income source changes the financial independence ratio significantly, it reduces the percentage of spending the portfolio needs to cover.

The practical implications of the ratio

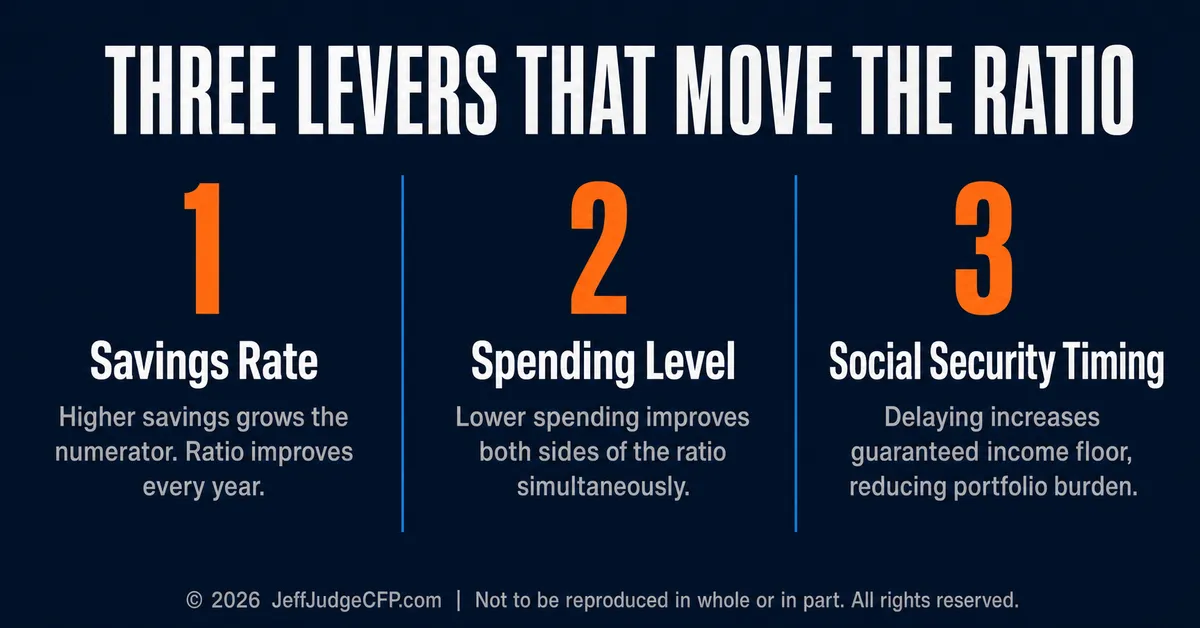

Once you know your ratio, the levers become visible.

The savings rate lever: every dollar added to the portfolio increases the numerator (portfolio-generated income) while, if lifestyle stays constant, keeping the denominator (spending) fixed. Increasing the savings rate by 5 percentage points can move the ratio by 3 to 7 percentage points annually depending on the starting portfolio size.

The spending lever: reducing annual spending improves the ratio on both sides simultaneously. It increases the percentage of spending the portfolio covers and reduces the total spending target that defines independence. Spending $150,000 per year versus $200,000 per year doesn’t just save $50,000, it changes the portfolio target required for independence by $1.25 to $1.5 million (at standard withdrawal rates).

The Social Security timing lever: delaying Social Security increases the monthly benefit, which increases the guaranteed income floor and reduces the percentage of spending the portfolio needs to cover. Per the Social Security Administration, delaying from full retirement age to 70 increases the benefit by 24%. For a high earner, that 24% increase on a meaningful benefit could reduce the required portfolio size by $200,000 to $400,000.

Why most people have never run this number

The financial services industry is built around accumulation. The messaging is about growing your portfolio, not about defining and measuring progress toward a specific independence threshold. Net worth is easier to market than the financial independence ratio.

There’s also a psychological resistance to knowing. Calculating the ratio reveals exactly where you are and exactly how far you have to go. That can be motivating or deflating depending on the gap. Most people prefer the ambiguity of “doing well” to the precision of “35% of the way there.”

But precision is what allows you to act. If you know you’re at 35% and need to be at 100% in 15 years, you know what trajectory is required. If you don’t know where you are, you can’t optimize the path.

Schedule a no-obligation call with Jeff to calculate your financial independence ratio and map what moves the number fastest.

,-

The information provided is for educational purposes only and should not be construed as investment advice. Investment strategies should be tailored to individual circumstances, risk tolerance, and goals. Past performance doesn’t guarantee future results. Consult with qualified financial professionals regarding your specific situation.

Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through Great Valley Advisor Group, a registered investment advisor and separate entity from LPL Financial.

© 2026 JeffJudgeCFP.com | Not to be reproduced in whole or in part. All rights reserved.

§